The municipal bond market, despite its long-standing reputation as a stable, tax-advantaged investment, currently presents a paradox for investors. On the surface, munis appear attractively priced, especially given their relative yields compared to U.S. Treasuries. Yet, beneath these appealing numbers lies a market grudgingly held back by a lack of clear catalysts—an environment simultaneously ripe with opportunity and riddled with uncertainty. This dissonance places municipal bonds in a challenging yet potentially rewarding position for the discerning, center-right investor.

Yield Disparities and Ratios: An Underappreciated Value Signal

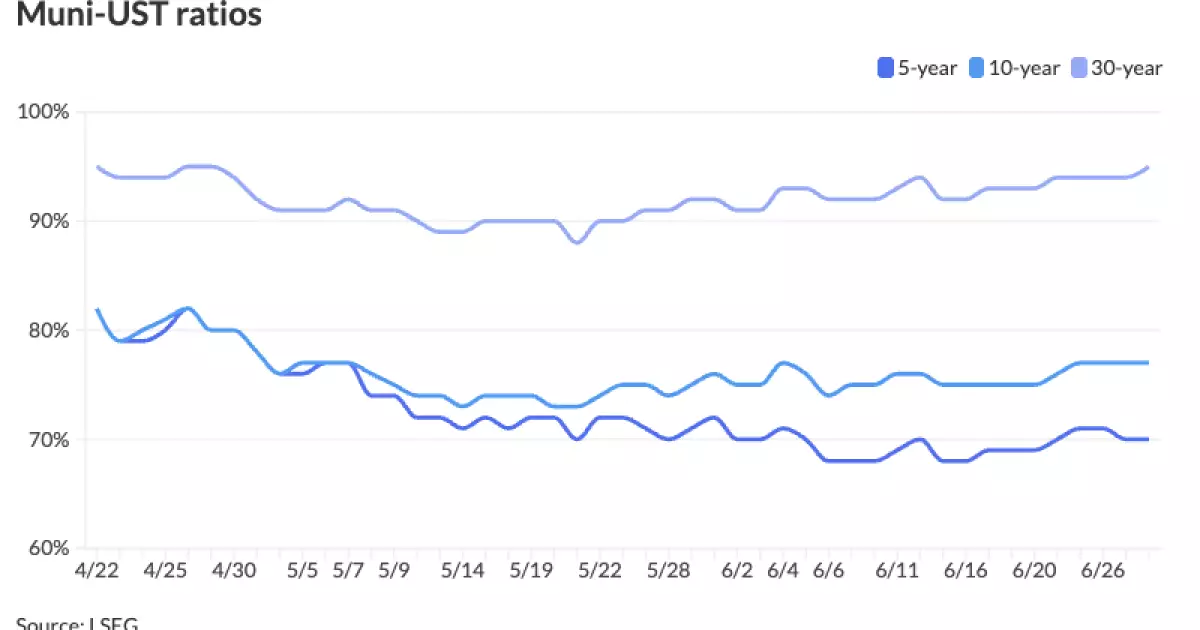

At first glance, municipal bond yields slightly edged higher this week, nudging up by a modest two basis points in contrast to falling Treasury yields that dropped by three to six basis points. The ratio of municipal bond yields to Treasury yields stands at around 70-95%, depending on the maturity. Reflecting a classic risk-reward scenario, munis offer yields that are still relatively cheap after considering the tax benefits. Particularly for longer maturities, the after-tax compensation appears generous—some high-grade bonds yield above 8% on a tax-equivalent basis. By conventional wisdom, this should ignite investor enthusiasm.

However, despite these seemingly attractive arithmetic signals, market behavior signals hesitancy. The ratios are drifting wider, implying that while municipal bond yields are rising or remaining stable, Treasury yields are falling. This divergence signals that investors remain skeptical about muni outperformance, a sentiment largely shaped by macroeconomic headwinds and subdued fund flows.

The Stubborn Absence of a Catalyst

One of the most frustrating aspects for municipal bond investors is the struggle to identify a meaningful trigger that could propel this asset class beyond its current languid performance. While there is an undeniable interest in “anything priced attractively,” dealers and strategists note that the primary market is stealing the spotlight, buoyed by strong demand and generous spreads. Yet, outside the primary market, the secondary market’s subdued volatility and minor price movements underscore a collective caution.

A major sticking point is that the fundamental drivers, such as sustained robust fund inflows, are missing their punch. Muni funds recorded inflows for the ninth consecutive week, but at a relatively diminished $76.9 million last week, nowhere near enough to ignite a true rally. For munis to outperform Treasuries meaningfully, fund flows need to accelerate dramatically—a condition currently unmet. The market’s “cheapness” continues to be noted, but the “fuel” to convert opportunity into performance gains remains absent.

Technical Strength Meets Political and Economic Ambiguity

From a technical perspective, municipal bonds are entering a period of increased cash flow, with July reinvestments swelling principal and interest returns to investors. Approximately $40 billion in principal and an additional $14 billion in interest payments are expected this month, a significant boost compared to previous months. This massive liquidity injection typically acts as a positive technical driver by providing a buffer against volatility and enhancing demand for new bonds.

Nevertheless, this is not happening in a vacuum. The market remains wary amid looming economic uncertainties and political considerations. States like California, New York, and Florida—giants in muni issuance and redemption—are steering significant volumes of debt activity, but the distribution remains uneven and cautious. Adding to the complexity, upcoming municipal bond sales in the weeks ahead involve large, selective deals rather than broad issuance events, indicating a continued tactical, rather than wholesale, appetite for municipal debt.

Primary Market Dynamics: The Lifeblood of Municipal Bonds

The primary municipal bond market remains the true “star” in current conditions, attracting investors with deals priced at wide spreads relative to Treasuries. This dynamic is crucial since the primary market sets the tone and provides liquidity for the often less-active secondary market. The heavy subscriptions and willingness of buyers to accept generous spreads reaffirm that munis retain their appeal under the right circumstances.

New issuance this week is relatively muted due to factors like the July 4th holiday but is expected to pick up significantly in the coming weeks, highlighted by major offerings such as California’s clean energy project bonds and New York’s hefty income tax revenue bond sales. These deals are shaping investor focus, selectively channeling capital into transformative infrastructure and environmental projects—themes that align well with a pragmatic, center-right outlook emphasizing sustainable growth and fiscal responsibility.

Why Central Banks and Fiscal Policy Matter More Than Ever

Central bank policies and federal fiscal strategy continue to exert profound influence on muni valuations. Municipal bonds, often viewed as safe havens with embedded tax advantages, are especially sensitive to changes in interest rates and economic uncertainty. Recent declines in Treasury yields should theoretically lift munis. Yet, risk aversion and yield curve dynamics have caused dislocations.

For the fiscally conscientious investor, the interplay between inflation, interest rates, and local government finance is vital. Rising interest rates can strain municipalities reliant on refinancing, while budget deficits linked to lingering pandemic-related expenditures may pressure creditworthiness. However, the resilience in fund inflows, even if modest, suggests that investors still value munis as a core portfolio component due to their favorable tax treatment and relative safety amid broader market volatility.

The Investor’s Choice: Embrace the Discomfort or Miss the Opportunity?

The current municipal bond market challenges investors to weigh patience against prudence. While yields appear enticing and technical factors project positivity, the absence of a clear performance catalyst tempers enthusiasm. The cautious tone is not a sign of structural weakness but rather reflects a transitional phase where the market awaits more definitive macroeconomic signals.

For the center-right investor focused on capital preservation and steady income, this environment requires strategic positioning rather than aggressive shifts. Selectivity, a keen eye for credit quality, and an appreciation for the nuanced relationship between munis and Treasuries will be paramount. Discomfort with market ambiguity may be the cost of entry, but the rewards on offer—particularly on an after-tax basis—urge investors not to misconstrue caution for complacency.