The municipal bond market is experiencing a complex interplay of variables that influence its stability and attractiveness to investors. As we near the end of the year, key fiscal indicators and market dynamics are prompting reflections on tax-exempt bonds, Treasury rates, and the overall economic climate. This article aims to unravel these trends and offer insight into how they might shape the future of municipal bonds.

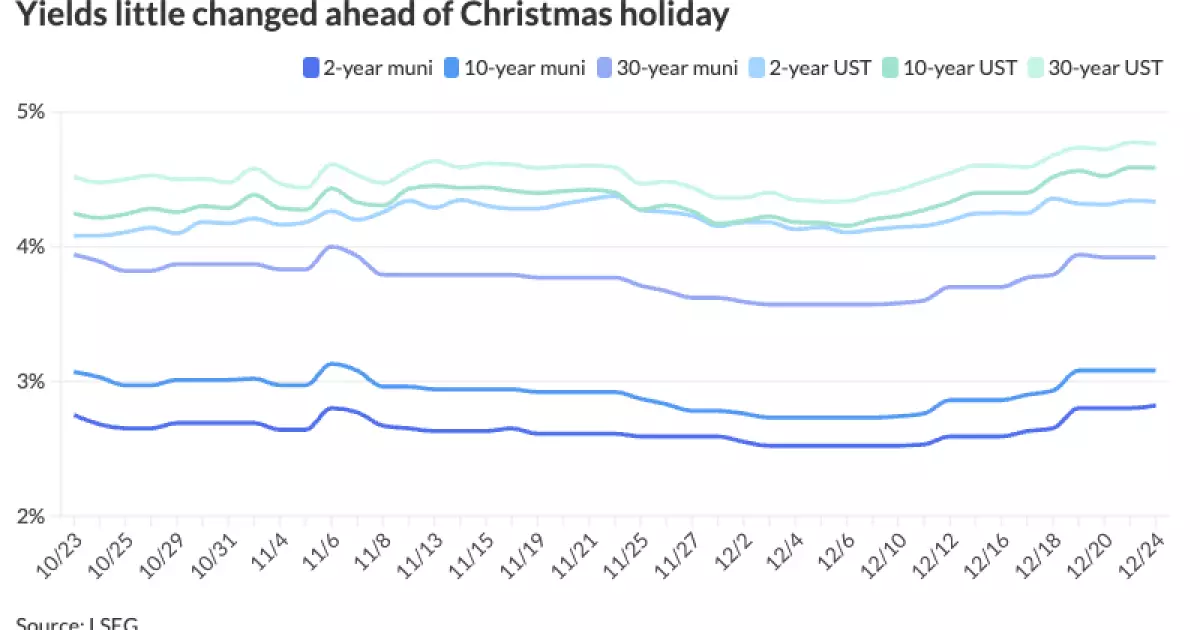

On a recent Tuesday, municipal bonds exhibited a mixed performance, with yields for high-quality bonds rising slightly while U.S. Treasury securities posted marginal gains. The slight upward movement of Triple-A yields by a basis point or two suggests growing investor caution amid fluctuating market conditions. This environment stands in contrast to the previous weeks, offering a unique glimpse into how external economic pressures can affect municipal bonds.

The ongoing strength of Treasury bonds is noteworthy. For instance, the two-year U.S. Treasury yield hovered around 4.60%, which is notably close to the higher yields observed in the spring months. When juxtaposed with tax-exempt municipal yields, which have been floating around 3.00%, the municipal-to-Treasury ratios show a mixed picture, with shorter maturities at about 65% and longer maturities at approximately 82%. Such ratios encapsulate the tension investors face in balancing risk versus return in their portfolio strategy.

Several macroeconomic factors are currently weighing on yield ratios in the bond market. According to Kim Olsan from NewSquare Capital, although taxable interest rates are under pressure, the municipal market exhibits strength, potentially indicating that investors are seeking stable safe havens in uncertain economic waters. This “supportive bidside” in the municipal market can often lead to increased purchasing activity, particularly for longer-dated bonds.

A notable development has been the significant withdrawal from tax-exempt money markets, with assets decreasing from a high of $137 billion to $132 billion recently. This shift indicates a strategic reallocation of resources by investors aspiring for higher returns. Interest rates for floating-rate bonds have also risen significantly, further reflecting investor movement towards the longer-end of the curve.

Growth in trading activities for longer maturities provides further insight into this trend, with a reported 67% of all secondary trades involving maturities beyond 2030. This focus on longer-term bonds suggests that investors are not only seeking the perceived safety of municipal bonds but are also capitalizing on the steepening of the yield curve which encourages extension of portfolios.

As we cast our gaze towards 2025, various factors will influence the municipal market. UBS strategists have issued a cautionary note regarding the heightened uncertainty surrounding fiscal and tax policy, particularly in an election year. With potential changes to the tax-exempt status of certain municipal bonds on the horizon, some investors may find themselves reassessing the sustainability of their bond portfolios.

Moreover, inflation remains a lurking concern. With anticipated increases in tariffs and a rise in fiscal deficit projected for 2025, some analysts believe that the resultant inflationary pressures could impact municipal credit ratings. Though fiscal hawks may moderate the extent of these shifts, municipalities could still feel the heat of rising costs and diminishing federal support.

Adding another layer of complexity is the infrastructure investment landscape. UBS anticipates tax-exempt bond issuance exceeding $450 billion next year, largely propelled by the need for upgrades and maintenance in aging infrastructure. This influx of supply acknowledges both the necessity for improvement and the grappling municipalities may face with dwindling fiscal resources.

The prospect of waning fiscal aid raises questions about broader credit risks for municipalities. As Cooper Howard from Charles Schwab points out, while many municipalities currently exhibit strong liquidity, the cessation of emergency funds from the American Rescue Plan poses a risk. Misallocation of these funds toward ongoing expenses could lead to significant financial difficulties when they run out, amplifying the need for careful fiscal management.

As we navigate the current landscape of municipal bonds, it’s imperative for investors to stay acutely aware of both macroeconomic trends and market dynamics. The interplay between Treasury rates, inflation expectations, and local fiscal health will likely define the trajectory of municipal markets in the years to come. As always, ongoing analysis and adaptation will be the keys to navigating this ever-evolving financial terrain.