In recent weeks, the municipal bond market has exhibited notable characteristics as it weathers varying influences from mutual fund inflows and shifting U.S. Treasury (UST) yields. On a particular Thursday, the performance of municipal bonds remained relatively stable despite broader fluctuations in equity markets and rising Treasury yields. Understanding the underlying demand for municipal debt, the evolving yield ratios, and the implications of increased issuance provides essential insight into current market conditions and investor sentiment.

According to data from Municipal Market Data, the yield ratios comparing two-year and longer municipal bonds with U.S. Treasuries displayed slight variances, with the two-year ratio at 62% and the 30-year at 86%. This relatively narrow gap suggests a complex interplay between municipal and Treasury yields, where investors are increasingly seeking out tax-exempt securities for better risk-adjusted returns amid rising interest rates. Kim Olsan, a senior fixed-income portfolio manager, emphasized that while Treasury yields moved upward, the municipal market remained insulated from these fluctuations, reflecting a stabilizing demand.

Pivotal to this stability is the observation that secondary markets have seen increased activity, particularly for maturities beyond twelve years—an indicator that investors are shifting preferences towards longer-duration securities to capture elevated yields. Such trends highlight a strategic adjustment from investors looking for enhanced return prospects. Interestingly, growth in munis traded with higher credit quality, such as state general obligations (GOs), alongside favorable market conditions, translates to competitive pricing.

Market participants have also observed a significant uptick in primary market activity. For instance, major issuances, such as the South Carolina Public Service Authority’s upsizing and New York City Municipal Water Finance Authority’s bond increase, suggest a robust appetite for municipalities to capitalize on favorable pricing and demand. This inclination towards larger issuances reveals how market dynamics can pivot in response to investor sentiment and the overarching economic landscape.

Olsan pointed out that upcoming expiration and redemption cycles could further influence market conditions. A projected negative supply, especially in robust states like New York and New Jersey, signals potential competition among in-state buyers. The absence of new issuances may drive investors toward existing tax-exempt credits, enhancing demand for those in the market while potentially destabilizing yields for other less-favored credits.

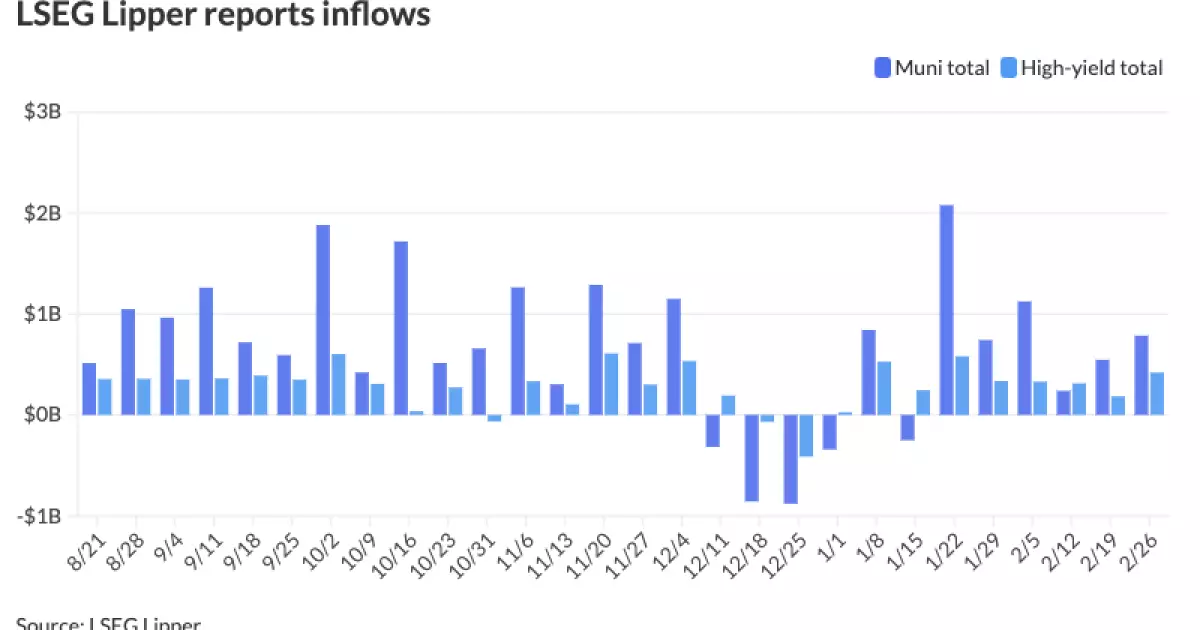

Recent fund flows illustrate a compelling trend toward municipal bond mutual funds, with an influx of $785.5 million over a recent week. This increase follows a steady inflow pattern of high-yield funds, underscoring a prevalent trend where investors prioritize tax-free income amidst broader economic uncertainty. Specifically, inflows recorded in high-yield municipal segments indicate a strategic pivot where investors seek higher returns presented by lower-rated securities amidst prevailing credit market constraints.

In sharp contrast, taxable money-market fund assets saw significant withdrawals. This divergence points to an increasing preference for municipal funds as tax-exempt investment opportunities gain appeal. The cumulative effect of these inflows strengthens the municipal market’s resilience, allowing it to balance out against broader Treasury and equity market volatility.

The current pricing landscape, as delineated by various yield scales, demonstrates a subtle yet significant evolution in investor behavior. For instance, as long-end maturities become increasingly attractive, notably with 30-year yields settling around or below traditional averages, investors may find themselves reassessing their portfolios. Pricing for high-quality long-dated securities, such as the Massachusetts Development Finance Agency and Florida Department of Transportation bonds, demonstrates an emerging context where relative value prompts strategic investment decisions across various maturity windows.

Moving forward, industry analysts anticipate that market corrections may breed further re-evaluations of allocation strategies, particularly in light of ongoing supply-demand imbalances. Furthermore, the mixed responses anticipated in credit spreads reinforce the notion that while certain segments may thrive, others could experience widening due to fluctuating supply.

The interplay of market conditions, including increasing inflows into municipal bond mutual funds and fluctuations in UST yields, shapes the current landscape of the municipal market. Key trends around longer-dated securities and adjustments to investor behavior reveal a crucial focus on yield opportunities amid a volatile financial environment. As we advance through the coming months, stakeholders will need to remain agile, continually reassessing strategies in response to a dynamic market characterized by changing supply conditions and investor sentiment. Understanding these variables will be critical for navigating the municipal bond market effectively.