The landscape of municipal bonds is currently marked by turbulence, as recent market indicators suggest further declines and a sense of hesitance among investors. Municipal bond yields are ascending, with steady yield increases observed throughout March, driven by a plethora of economic headwinds and fundamental weaknesses. The disparity between municipal bonds and U.S. Treasury (UST) yields portrays a troubling trend; this rising yield scenario is surely a cause for concern. In this context, one must not only evaluate the numbers but also grasp the underlying implications of these movements on local economies and public trust.

The Ratios Tell a Story of Divergence

Analyzing the ratios of municipal bonds to USTs provides crucial insights into market sentiment. As of Thursday, the two-year municipal to UST ratio hovered around an alarming 69%, while the longer-term bonds maintained a ratio that rose, topping 91% for 30-year bonds. This divergence showcases a critical market reality: municipal bonds are yielding higher returns relative to UST bonds, but at a cost—this cost is tied to perceived risk in local governance. A ratio that should ordinarily reflect confidence is instead signaling concern, as the foundations of municipal funding come under strain from external economic forces and local budget crises.

Examining the Rising Yields

The implications of rising yields in the muni sector are manifold. Investors are confronting an inversion of expected returns. The municipal yields have risen significantly; for instance, the AAA-rated credits are now approximately 60 basis points higher than six months ago. This trajectory not only raises alarms for individual investors but casts shadows upon local governments relying on bond markets for critical funding. The present reality reveals that municipal bonds are now climbing above levels typical for mid-2023 which were neither sustainable nor indicative of healthy fiscal policy.

A concerning observation made by experts like Kim Olsan highlights this trend, emphasizing that both UST and municipal securities are aligned in agreement: rising yields dominate the narrative. This acknowledgment encapsulates the current market sentiment where investors are relegating opportunities to yield rather than overall market quality. It underscores a broader trend of investors seeking out higher-rate opportunities while grappling with the increased risk that accompanies such decisions.

Challenges in Dealer Inventory

The present market dynamics present unique challenges for dealers, as inventories have surged to their highest levels since December 2023. These high inventory levels complicate market transactions, emphasizing the struggle dealers face as they attempt to distribute an ever-increasing volume of munis. Olsan’s observations speak volumes about the underlying trends in market dynamics, remarking on how increased inventories bring about a “major challenge” for issuance and pricing in what ought to be a more stable environment.

Potential Opportunities Amidst Adversity

Despite the overarching sense of gloom that is assailing the municipal bond market, there are still glimmers of opportunity. The existence of high-grade credits that exceed 5% TEYs amidst rising interest rates reveals that there are indeed value-seeking investors poised to capitalize on returns that may not last. The emergence of 5.00% or more in TEYs presents a stark contrast to previous periods and suggests that strategic investors who keep an eye on the nuances of coupon structures could emerge successfully from these turbulent times.

The Outlook for Investors and the Broader Market

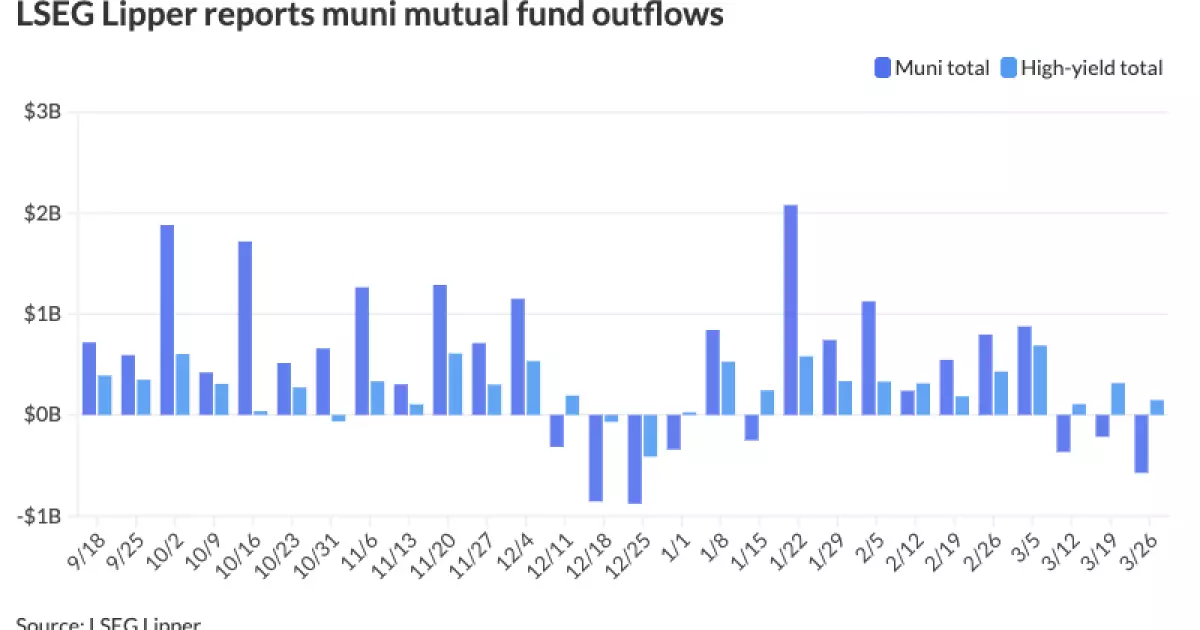

As investors withdraw substantial funds—reporting outflows of $573.3 million last week alone—the possibility of a broader sentiment shift further complicates the landscape. The fear of continued losses leaves a lasting impact, weighing on public-sector funding and stymieing growth strategies that rely heavily on bond financing. The general sense that municipal bonds are becoming more volatile cannot be overlooked; when investors steadily withdraw, it raises critical questions about the robustness of local economies and their ability to meet fiscal challenges in the near future.

The paradox emerges that although investors may find bonds appealing due to higher yields, the existential risk for municipalities must be acknowledged. With the average tax-free municipal money market fund yields falling against increasing taxable money-fund yields, there is a visible dissonance in investor behavior that raises numerous concerns.

Fundamentally, the municipal bond market stands at a crossroads. As rates rise and public trust wanes, the precarious balance that municipal governance seeks to maintain between fiscal responsibility and investor confidence looms larger than ever. In the face of possible economic downturns, the burden lies heavier than perhaps any time in recent history, and as investors navigate these challenges, the role of strategic foresight cannot be overstated. The key elements shaping the near future will revolve around adaptability, informed decision-making, and an understanding of the intricate dynamics at play within the municipal bond arena.