The U.S. municipal bond market, often perceived as a safe haven for conservative investors, is currently grappling with contradictory signals. In the first half of 2025, the market saw unprecedented issuance levels, with total supply already surpassing $275 billion and projections rising above $580 billion for the year. While such robust supply traditionally signals strong demand and market health, the reality is far less encouraging: despite record issuance, municipals have underperformed significantly, posting negative total returns year-to-date—the sole fixed income segment to do so. This disconnect hints at underlying structural and sentiment issues that deserve a more critical look from investors who still consider munis a cornerstone of a balanced portfolio.

Supply Glut and Its Consequences

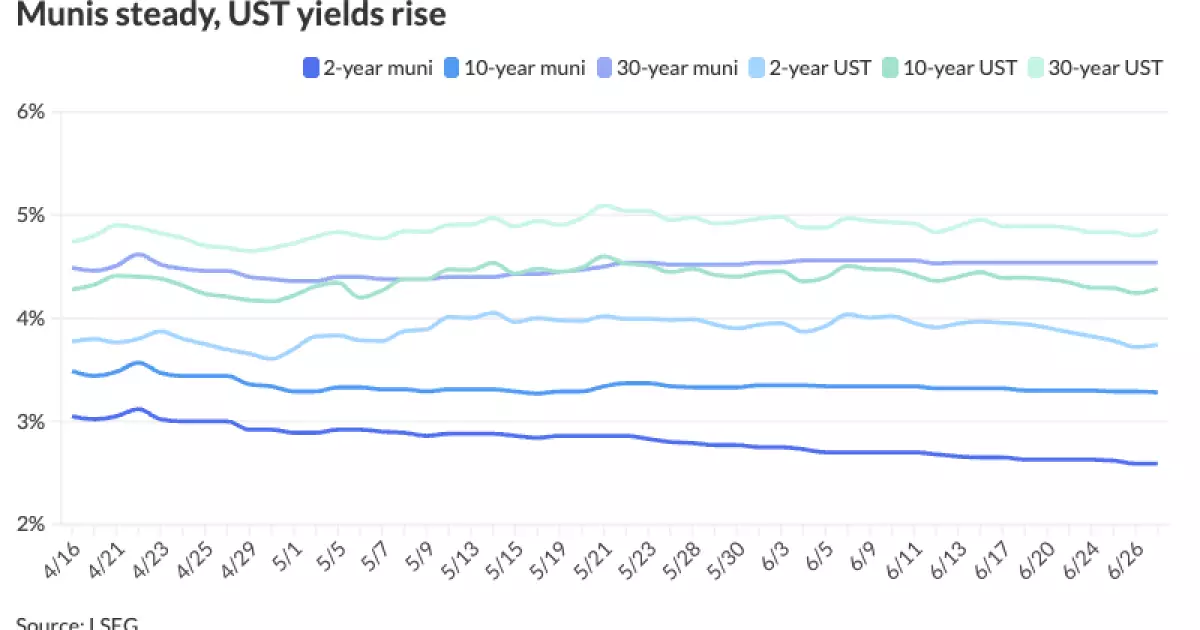

One cannot overlook that June marked the largest single month for municipal issuance in 2025, topping $50 billion. Yet this flood of new bonds has burdened the market rather than invigorated it. Typically, a supply surge might ignite demand from investors chasing yield. However, tax-exempt munis have lagged Treasuries in performance notably this month, stretching muni-to-Treasury yield ratios to unattractive levels—77% for 10-year maturities and nearly parity at 94% on the 30-year tenor. This underperformance reflects not just oversupply but also investor reluctance to absorb bonds amid concerns over rising interest rates and credit quality uncertainties.

Barclays strategists’ observation that valuations look “good” at such historical lows might be overly optimistic. If prices are depressed not by temporary dislocations but more persistent structural forces such as increases in municipal debt burdens or shifting federal policies, then the “value” could be a reflection of rising risk rather than opportunity.

The Myth of Strong Summer Performance

Seasonality has long been a pillar of muni market analysis, with historically stronger performance expected in July and August fueled by bond redemptions and coupon flows. Barclays and Bank of America strategists predict this trend will continue, painting a sanguine picture for the remainder of the summer. While it is true that coupon payments and redemptions offer natural demand support, putting too much faith in seasonal cycles can be a trap. With issuance forecasted to remain elevated and economic uncertainties lingering—such as inflation concerns and potential shifts in tax policy—expecting past patterns to hold without considering the broader macro context is naive.

Moreover, optimistically projective comments about a “breather” in supply fail to account for a shifting investor base. The gradual withdrawal of retail and the cautious stance of institutional buyers, wary of rising rates and fiscal imbalances at state and local levels, could mute the canonical seasonal strength that has supported munis historically.

The Role of Rising Treasury Yields and Market Dynamics

Treasury yields have risen across the curve in recent weeks, with the two-year Treasury hitting 3.745% and the 30-year creeping toward 4.846%. This rise has put additional pressure on tax-exempt yields and compressed the spreads that muni investors rely on for tax advantage. When Treasuries become more attractive, even with higher federal taxes looming, muni bonds must either compete on yield—which is becoming increasingly expensive for issuers—or face outflows.

The recent increase in yields, coupled with wider muni-Treasury ratios, signals a precarious balancing act. Investors demand higher yields on municipals to compensate for perceived risk and despite the tax-exempt status. But this dynamic can reactivate a vicious cycle: higher yields increase borrowing costs for municipalities, potentially exacerbating credit risks especially for entities with weaker fiscal positions, which in turn could further spook investors.

An Overly Rosy Forecast from Market Strategists

Perhaps most concerning is the prevalent tone of cautious optimism from major strategists like those at Barclays and BofA. Their bullishness—grounded in historical patterns and supply-demand technicals—appears detached from hard realities on the ground, notably the mounting debt burdens borne by municipalities and the uncertain trajectory of fiscal federal support.

The argument that munis are “the only fixed income asset class with negative total returns” lends itself nicely to a contrarian call of “value,” yet ignoring underlying economic and political risks may prove perilous. Local governments continue to face inflation-driven increased costs, particularly in labor and infrastructure, while federal aid has become less predictable following pandemic-era stimulus. This landscape does not suggest a market poised for a robust, uninterrupted recovery in the back half of 2025.

What Investors Should Really Consider

From a center-right, fiscally conservative perspective, the municipal market’s troubles highlight a broader problem in American fiscal federalism—the chronic underfunding and excessive borrowing of local governments, which taxpayers and investors alike will pay for sooner or later. The rising supply is a symptom of political unwillingness to control spending rather than a market phenomenon that can be remedied through mere adjustments in timing or seasonality.

Investors should be cautious, not complacent. The best path forward involves demanding greater transparency and accountability in municipal finances and questioning the sustainability of ever-increasing issuance. Blindly chasing yield or assuming that summer seasonality will reverse negative trends ignores the very real risks facing municipalities in a higher-rate environment.

In a landscape defined by ongoing fiscal strains, rising borrowing costs, and shifting investor preferences, recognizing the persistent weaknesses in the municipal bond market is essential—not just acknowledging fleeting technical factors or cyclical patterns. The narrative of steady recovery and undervaluation hides a more complex and less optimistic reality for one of America’s traditionally safest asset classes.