In a landscape where most asset classes rally in response to shifting Federal Reserve policies, municipal bonds have stubbornly refused to participate, revealing a troubling divergence. While equities reach for new heights and corporate bonds benefit from decreased yields, munis are quietly declining, exposing underlying vulnerabilities unlikely to resolve without significant market upheaval. This dissonance should alarm investors and policymakers alike, as it hints at structural issues that threaten to undermine the stability of local governments and the broader financial system.

At first glance, municipal bonds seem to be performing with a shrug—little change in prices and ongoing yield adjustments. But beneath this superficial calm lies a tumultuous story of overissuance, investor aversion, and rising economic headwinds. The muni market’s recent trajectory diverges sharply from other fixed-income assets, with the long-term muni index down almost 4% year-to-date. This underperformance is not merely a temporary anomaly but a sign of deeper structural strain.

What makes this situation more alarming is the disconnect between supply and demand. States and municipalities flooded the market with $280 billion of new bonds in the first half of the year—a response to fears that the removal of tax exemptions would cripple their borrowing capacity. Yet, with the tax exemption retained—thanks to legislative action—the anticipated rush has cooled, leaving a market with excess supply that no longer has the immediate urgency to absorb new issuance. This surplus, combined with inflationary pressures hiking the cost of capital projects, has created a perfect storm for muni securities.

Investors have responded by shunning longer maturities, preferring to stay within shorter-term assets that offer more predictable returns. The steepening of the muni yield curve, especially at the long end, underscores this risk aversion. It signals growing concerns about the ability of issuers to meet their obligations or the likelihood that future economic conditions could force municipalities to tighten their budgets even further. The question remains whether this is a temporary consequence of market oversupply or an ominous sign of deeper, potentially insoluble structural issues.

Market Dynamics: Is There a Tipping Point Ahead?

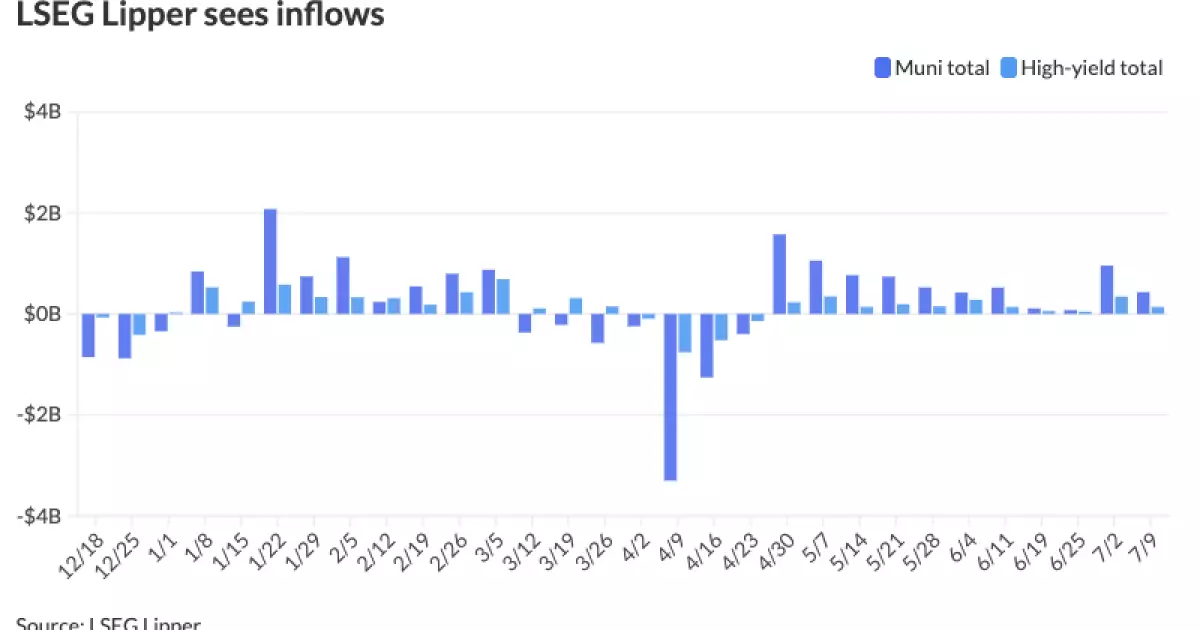

The recent shifts in fund flows reinforce the narrative of uncertainty. Investors increased holdings in municipal bond funds by over $430 million, yet there’s unequivocal reluctance to extend maturities beyond 15 years. This bifurcation—protecting short-term liquidity while shunning long-term risk—is a red flag indicating that the market perceives an increased likelihood of future shocks. The unwavering preference for shorter durations suggests a widespread expectation that longer-term munis could become riskier or less liquid as economic pressures mount.

Furthermore, the upcoming rate environment is pivotal. If the Federal Reserve begins cutting rates in the fourth quarter, as some speculate, the resulting rate rally would likely buoy municipal bonds. Lower borrowing costs could alleviate some of the pressure on municipalities, possibly calming the curve and correcting recent underperformance. However, this optimistic scenario depends on the resilience of the broader economy and political support for fiscal stability—areas where uncertainties abound.

The role of supply cannot be understated. Having frontloaded issuance during the first half of the year to hedge against tax changes illustrates how legislative fears can distort market behavior. Now that uncertainty about tax exemptions is largely resolved, a slowdown in issuance is conceivable. Yet, whether this will reverse the current trend remains in question, especially as inflation, pandemic-related backlogs, and increased project costs continue to weigh on local government finances.

Are these market dynamics merely a cyclical correction, or do they signify a more enduring structural transformation? The steepening yield curve, declining long-term muni prices, and investor reluctance all point toward a paranoid outlook favored by a skeptical investor base. This skepticism could deepen if political, economic, or fiscal uncertainties persist, challenging the assumption that munis are inherently safe or immune to systemic shocks.

The Broader Implications for Investors and Policymakers

The greater concern lies in the potential for this munis’ underperformance to spill over into broader financial stability. Historically treated as safe havens, municipal bonds now appear vulnerable to a shift in investor sentiment—especially if economic growth stalls or credit pressures increase. Given that munis represent a significant portion of conservative portfolios, their underperformance could trigger a reassessment of risk models and asset allocations across the board.

Policy responses will have to be swift and nuanced. If the Federal Reserve signals future rate cuts, it could do more harm than good if it fuels a short-term rally that masks deeper vulnerabilities. Conversely, remaining hawkish might exacerbate the muni market’s distress, making borrowing more expensive for localities and further dampening economic growth at the municipal level.

Critical to this evolving scenario is how investors interpret the ongoing divergence within fixed-income markets. Can the muni market reassert itself, or will it remain an outlier, signaling a more profound shift in the perception of risk? The current environment suggests the latter, with a real possibility that these anomalies foreshadow a broader recalibration of risk across the financial landscape.

The truth is that the muni market’s recent behavior exposes the fragility of fiscal confidence at the local level. When liquidity dries up, or when long-term bonds lose value, the repercussions are not contained within municipal portfolios—they ripple outward, threatening the integrity of the broader bond markets and investor trust. For those standing at the crossroads of economic policy and market stability, this signals the need for vigilant oversight, prudent risk management, and a healthy dose of skepticism about the narrative of perpetual safety that has long surrounded municipal bonds.