Despite recent reports suggesting a period of tranquility in bond markets, a deeper analysis reveals underlying fragility that is often glossed over. U.S. Treasuries and municipal bonds may have experienced modest price adjustments and slight yield increases, but these superficial fluctuations mask a precarious landscape that could unravel unexpectedly. Market participants, seduced by the illusion of stability, are overlooking warning signs that signal a potential shift to volatility. This complacency could prove costly, as the notion that markets are “overdone” and in need of a pause ignores the persistent structural risks and systematic vulnerabilities building beneath the surface.

The so-called “quiet” market merely signifies a lull before the storm, driven not by genuine financial health but by short-term tactical maneuvers and technical factors. While some analysts, like Tim McGregor, anticipate a pullback, their outlook merely reflects market tide-turning behaviors rather than fundamental strength. In reality, the tapering of exuberance and the slight rise in yields—up to four basis points—are indications of emerging tension, not resolution.

Disparities Between Perception and Reality in Yield Ratios

The large disparities in muni-UST ratios highlight the disconnect between perceived safety and actual risk. With ten- and thirty-year ratios hovering near 70% and 90%, respectively, investors are deluding themselves into believing that municipal bonds are cheap relative to U.S. Treasuries. This narrative of “good returns” and “positive momentum” obscures the fact that these spreads could widen rapidly if interest rate dynamics shift or fiscal fundamentals deteriorate.

High-yield munis, which have gained approximately 1.68% YTD, might seem attractive compared to other fixed income assets, but they carry amplified risks. The popular chase for higher yields contributes to inflated prices, which are increasingly vulnerable to a correction if macroeconomic conditions falter or if inflation pressures resurface. The optimism around tax-exempt munis’ outperformance risks becoming a mirage, hiding the potential for losses should the market experience a sudden change in appetite.

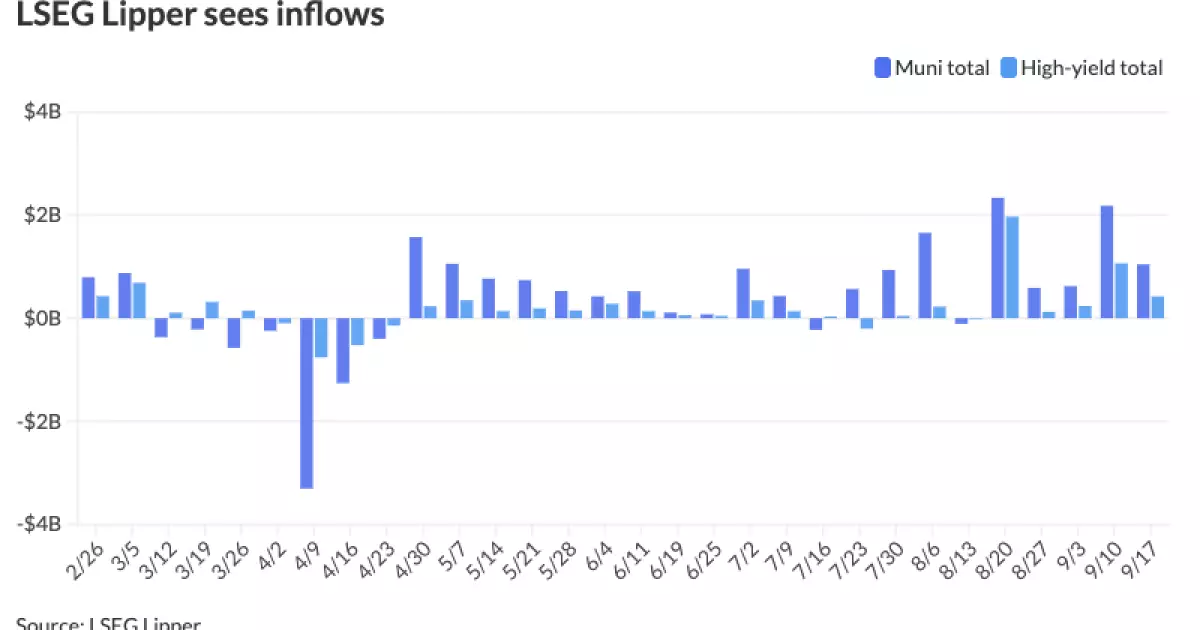

The Myth of Loose Supply and Sufficient Demand

While supply has been described as “manageable,” the notion that future supply will remain benign is overly simplistic. Market professionals warn of a significant pickup in issuance in the fall, which could flood a market already stretched thin by extraordinary inflows. The inflows into municipal funds—over a billion dollars in a recent week—are largely driven by retail investors seeking safe havens for their capital. Such flows, however, are a double-edged sword: they inflate asset prices and obscure underlying vulnerabilities.

In particular, the divergence between demand for long bonds and the actual supply dynamics creates an environment ripe for overvaluation. When the market finally confronts a supply glut or a shift in investor sentiment, the illusion of robust demand may quickly erode, precipitating a sudden and sharp correction. The latest figures on CUSIP requests and bond issuance underscore a mounting pressure point that investors and policymakers are ill-prepared to absorb.

The Underlying Danger of Fluctuating Yields and Valuations

Market metrics such as the AAA yield curves and bond slopes reveal a scenario where valuations are increasingly detached from fundamentals. The steepness of the muni curve—more than double that of UST yields—suggests a landscape where long-term bonds have been overly extended. Quick gains in long-term indices, such as those exceeding 4.5% in September, are not signs of sustainable growth but of speculative excess that could reverse abruptly.

Furthermore, the ever-present threat of inverted curves—particularly within the five-year to ten-year span—hints at looming economic headwinds. The fact that yields at or below 2% for AAA-rated bonds are being justified by market optimism ignores the potential for rising rates or fiscal shocks that could quickly render these valuations as unsustainable. Local issues, such as the Georgia GO sale at 2.01%, exemplify the delicate balancing act between attractive valuation and realistic pricing.

The Paradox of Stable But Fragile Fund Flows

The current pattern of fund flows further exposes the fragility hidden behind perceived market calm. Although municipal funds have experienced significant inflows, including a recent $1 billion addition, this momentum masks the underlying risk buildup. Investors are attracted primarily to the safety profile of tax-exempt bonds, but their eagerness can lead to overconcentration and distorted prices. The recent outflows from tax-exempt money market funds, coupled with rising yields, reflect investor apprehension about liquidity and potential future volatility.

The stability of the SIFMA Swap Index at around 2.70% masks underlying liquidity issues, as dealer inventories have remained stable only superficially. Such stability may be temporary, especially if macro conditions shift or if policymakers lose control over inflation and interest rate expectations. The complacency stemming from these calm periods is dangerous, as it fosters a false sense of security among investors who are unaware of the accumulating risks.

The Harsh Reality Behind the Data

The seemingly benign data records—such as increased CUSIP requests or marginal yield cuts—should not lull investors into a false sense of confidence. These figures, when viewed in context, reveal a market teetering on the edge of correction. The surge in municipal issuance and the persistent pursuit of yield, especially in longer maturities, risk creating a bubble that could burst with little warning.

The very structure of the current fixed income landscape—characterized by artificially low yields, inverted curves, and outsized demand—screams warning signs. While policymakers and market participants may trumpet the stability of the moment, the underlying vulnerabilities—overleveraged positions, inflated valuations, and the looming threat of rate hikes—are evidence that this equilibrium is fragile at best. The market’s steady march forward may appear resilient, but beneath that surface lies the potential for a rupture waiting to happen.