The municipal bond market has recently experienced notable shifts, particularly as yields demonstrated a decline on Thursday, effectively ending a series of four consecutive trading days marked by increasing rates. In tandem with a modest improvement in U.S. Treasuries, municipal equities exhibited mixed performance, indicating varying investor sentiment and market reactions.

Municipal yields fell by as much as seven basis points, with variations dependent on maturity scales. For instance, two-year municipal bonds were reported at a ratio of 66% relative to U.S. Treasuries (UST), while longer durations like the 10-year and 30-year saw ratios of 72% and 87%, respectively. This slight decline in Muni-UST ratios suggests a narrowing gap as investors assess the shifting landscape of yield opportunities.

Market monitoring services such as Refinitiv Municipal Market Data noted these adjustments at 3 p.m. EST, which could reflect investor reactions to broader economic indicators. The reduced yields come as a departure from the preceding weeks where yields had been rising, indicating a potential recalibration of expectations regarding economic growth and interest rate movements.

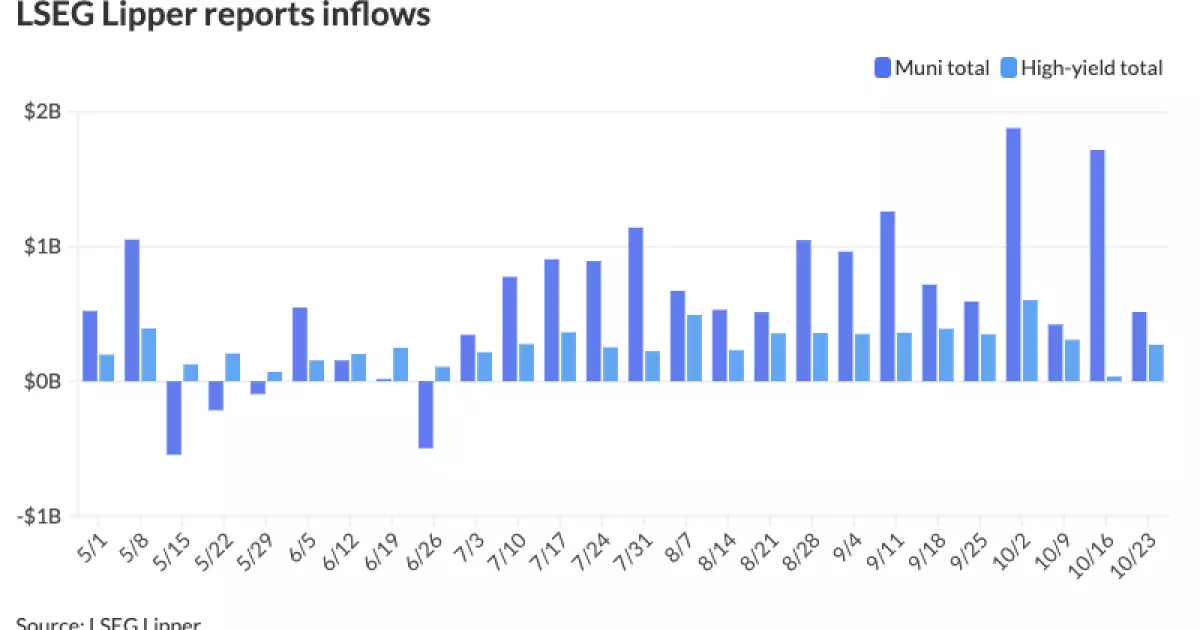

Despite the recent downturn in yields, the trend of positive inflows into municipal bond funds has persisted. Recent data from LSEG Lipper reveals that investors allocated $514.7 million into municipal bond mutual funds in the week terminating on Wednesday. While this amount is substantially lower than the previous week’s inflow of $1.718 billion, it still highlights a strong commitment among investors, marking 17 consecutive weeks of positive inflow trends.

Further dissecting this trend, high-yield bond funds have seen an upswing in inflows, which increased from $36.2 million the week prior to $271.8 million. Such inflows are largely attributed to investors seeking favorable returns, a pattern grounded in the positive performance seen from June to September. However, with October yielding an overall negative return of 1.88%, year-to-date returns have been constrained to a mere 0.37%. Investment experts like Sheila May from GW&K Investment Management suggest that recent economic reports have led to some cautious reassessment but do not indicate a monumental shift in investor confidence.

The ongoing discussions around potential Federal Reserve rate cuts have significantly impacted the municipal bond landscape. While earlier anticipations pointed towards the Fed lowering rates two more times this year, robust employment data and consumer spending figures have shifted this perspective. May articulated that the allure of returning to previous rate cut expectations is now “off the table,” underscoring a need for investors to remain vigilant to changes in monetary policy that could influence municipal bond yields.

Strategists at Principal Asset Management have suggested that while underlying fundamentals remain strong—with credit upgrades significantly outpacing downgrades—technical factors have recently been less favorable for the municipal bond market. The considerable increase in bond issuance, marked at $418.451 billion year-to-date—a striking 41.1% rise—signals with growing infrastructure needs and fading federal aid.

The demand for infrastructure financing continues to drive municipal bond issuance. Experts acknowledge that sectors such as healthcare and educational institutions are seeing increased bond sales, which may reflect a more sustained demand for capacity-building investments rather than a transient pre-election impact. Analysts have pointed to an estimated $1.2 trillion in deferred maintenance particularly in water utilities, with an additional $1 trillion needed for higher education upkeep.

Several weeks of issuance exceeding $10 billion have illustrated a broader trend, with significant interest in deals providing additional income spread. This suggests not only a reactive market but one that is attracting investors looking for stability and returns amid fluctuating climate conditions. As the market approaches the holiday season, more issuers are expected to target opportunities to capitalize on favorable borrowing conditions.

With projected robust deal pipelines and potential for record issuance in 2024, market participants are keeping a close eye on developments post-November 5, as the dynamics of supply could alter leading into the Thanksgiving and Christmas periods.

In the primary market Thursday, notable transactions included the pricing of tax-exempt power supply revenue bonds by Goldman Sachs for the Intermountain Power Agency and the Lifebridge Health Issue revenue bonds by BofA Securities, indicating continued robust demand for high-quality municipal placements. As seen in the performance of these deals, market appetite remains strong, reflecting an overall confidence in the municipal sector.

The municipal bond market is navigating a complex interplay of declining yields, ongoing investment inflows, and a ripe environment for sustained issuance driven by infrastructure needs. Investors and analysts alike must remain attuned to both economic indicators and market dynamics as they continue to unfold, shaping the future landscape of municipal finance.