The landscape of the municipal bond market is continually evolving, shaped by a complex interplay of economic factors, interest rate fluctuations, and market sentiment. As of late August 2023, municipal bonds are demonstrating a stabilizing trend amidst varying performances in the U.S. Treasury and equities markets. This article provides a detailed analysis of current municipal bond movements while underscoring significant implications for investors and the market at large.

Recent observations reveal that municipal bonds have remained steady, while U.S. Treasury yields exhibit slight weakness. This dichotomous behavior indicates a resilience in the municipal market, which can often be juxtaposed with shifting economic conditions. For instance, the municipality-to-Treasury yield ratios have characterized this period. Currently, the two-year ratio stands at 62%, while the ratio for the 30-year muni is recorded at 87%. These ratios, paired with Refinitiv Municipal Market Data, illustrate a continuing attractiveness of municipals despite slight fluctuations in the broader market.

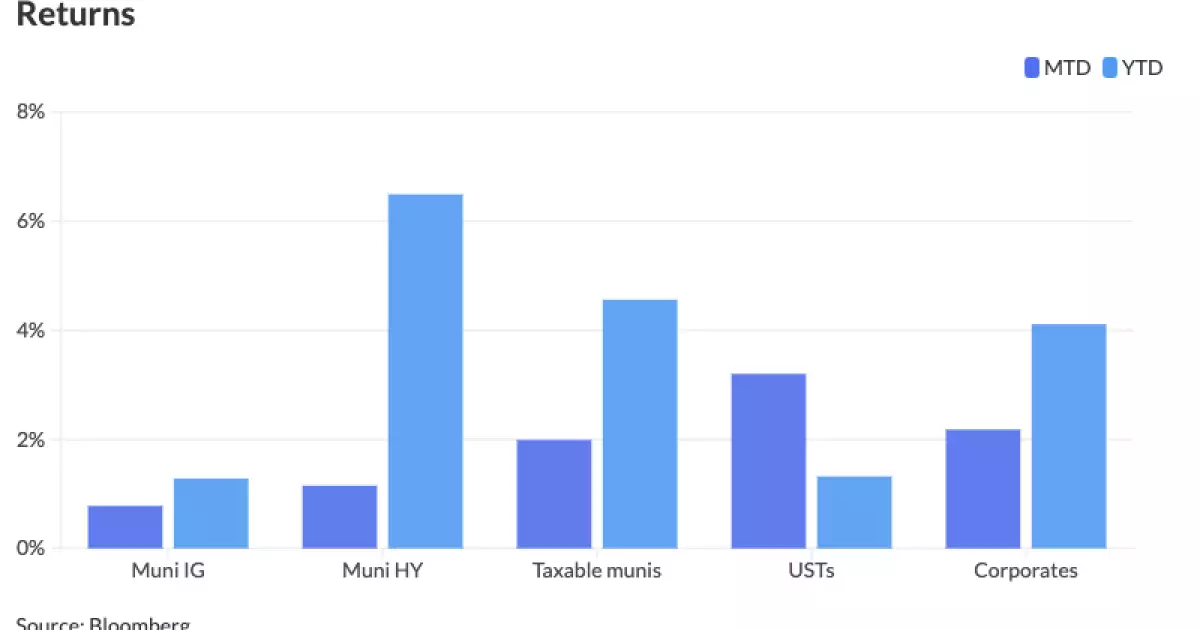

Moreover, this steady performance is significant as it comes after tumultuous times for the municipal segment. In August of the past year, the market faced losses averaging 1.79% as the Federal Reserve maintained its aggressive rate hikes to combat escalating inflation. This year, however, the narrative has shifted dramatically; municipalities are now enjoying gains of approximately 0.78% for the same month, culminating in a year-to-date return of 1.28%. Such a stark reversal underscores how quickly market sentiments can turn, often based on the responses of key regulatory institutions like the Federal Reserve.

The landscape of municipal yields has experienced notable shifts throughout August 2023. On average, municipal yields have increased by 26 basis points across various maturities, with the 10-year notes experiencing a rise of around 36 basis points. Yet, month-to-date observations reveal a slight decline of 2.5 basis points from the 10-year yields, primarily influenced by forward-looking policies hinted at by Fed Chair Jerome Powell.

The connection between Powell’s policy adjustments and market reactions cannot be overstated. As he indicated the potential for rate cuts, investor sentiment shifted, resulting in Treasury yields falling sharply and equities rising. This response reflects a critical trend where bond markets react not just to changes in interest rates but to the sentiment and anticipatory actions of market participants regarding fiscal policy alterations.

As summer wanes and the Labor Day holiday approaches, the municipal market experiences a characteristic slowdown. This seasonal dip can be attributed to various factors, including vacation schedules and general market inactivity. However, the potential of heightened activity looms on the horizon, particularly with a forecast showing above-average issuance in the weeks to come, primarily from significant entities aiming to refinance or fund essential projects.

Market commentators have noted recent catch-up movements in response to Powell’s speech, indicating a revitalized interest in the secondary market, particularly at the longer end where the 30-year muni ratios approach 90%. This uptick suggests that investors are cautiously optimistic, positioning themselves for potential gains as economic conditions unfold.

Looking ahead, the primary market features an array of noteworthy issuances. For example, the North Texas Tollway Authority plans to issue $1.1 billion in revenue refunding bonds, along with several other substantial deals across various states. The infusion of fresh capital through these bond issuances signals a sustained confidence in municipal finance, despite the backdrop of fluctuating yields and evolving fiscal policies.

Such activities not only bolster liquidity in the municipal market but also reflect wider economic health, as municipalities increasingly leverage bond markets to fund infrastructure and service projects. This is particularly relevant in the context of maintaining and upgrading essential community services and infrastructure.

The AAA yield curve remains stable, indicating a balanced outlook for municipal issuances. Current yields across various maturities, such as the one-year and 30-year, exhibit stable figures, reinforcing the notion of a steady market amid potential future volatility. Investors are encouraged to remain vigilant and informed, particularly as upcoming economic data and Fed communications could prompt further fluctuations.

The current municipal bond market displays a cautiously optimistic demeanor, characterized by stability despite external pressures. As investors navigate these waters, they must weigh both current performance trends and future market expectations, acknowledging that shifts can occur rapidly in response to economic signals and fiscal policy changes. Engaging with this dynamism while remaining attuned to emerging trends will be crucial for guiding investment strategies in this evolving landscape.