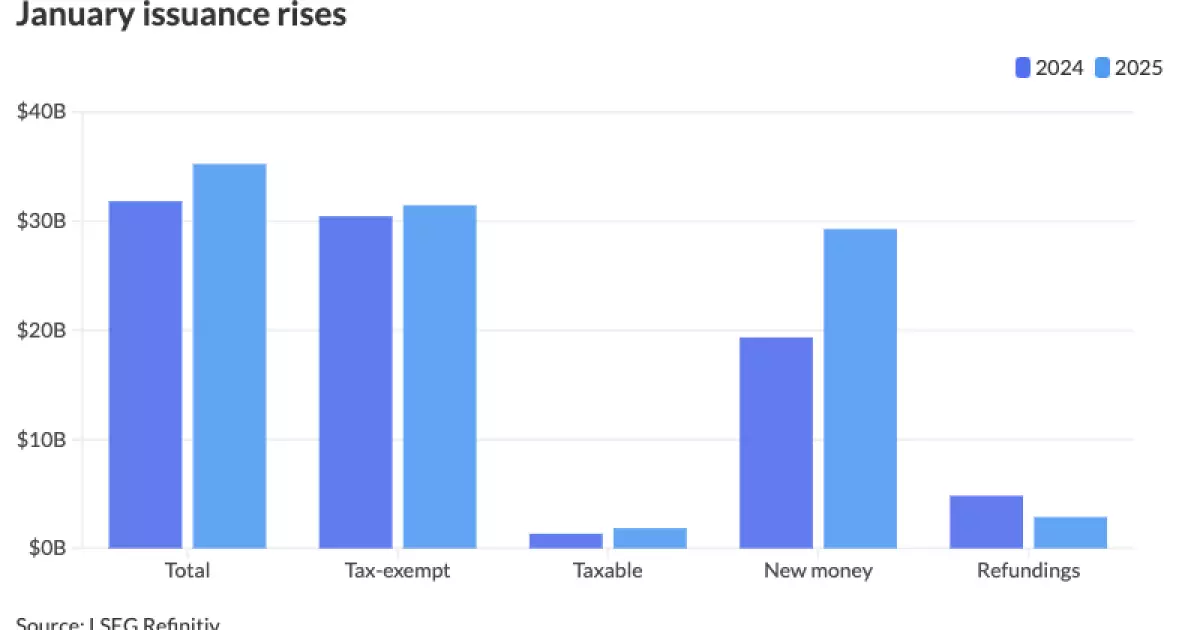

The municipal bond market experienced a notable upswing in January 2025, characterized by a year-on-year increase in issuance that has sparked significant interest amongst investors and analysts alike. According to the latest data from LSEG, the total issuance for the month reached an impressive $35.243 billion across 486 distinct issues, marking a 10.8% growth from the $31.817 billion associated with 554 issues during the same period in 2024. This surge not only indicates a robust start to 2025 but also exceeds the historical ten-year January average of $28.675 billion, reflecting a climate of heightened activity amid potential economic shifts and policy changes.

Several factors contributed to this increase in municipal bond issuance. Foremost among these is the prevailing sense of urgency among issuers to capitalize on favorable market conditions before anticipated fiscal and monetary policy adjustments could potentially disrupt the landscape. Alice Cheng, a credit analyst at Janney, identified the Federal Open Market Committee (FOMC) meeting and the federal interest rate decisions as significant influences. Despite the Federal Reserve maintaining rates within the 4.25% to 4.50% range, there remains a backdrop of pressure from political figures for potential rate cuts, thereby introducing additional volatility to market conditions.

Furthermore, concerns among issuers regarding the future use of funds from the Infrastructure Investment and Jobs Act have prompted them to act promptly, necessitating immediate access to capital markets rather than delaying decisions in an uncertain environment. Cheng posits that such apprehension extends to the tax-exemption status, particularly with regards to healthcare and private university institutions, compelling issuers to move swiftly to safeguard against future funding restrictions.

The municipal bond market is currently navigating a complex scenario marked by high interest rates and a disproportionate influx of funds across mutual funds and exchange-traded funds (ETFs). This dichotomy creates a unique investment environment where issuers must balance the risks associated with high rates against the clear and urgent need to fund capital projects. James Pruskowski, chief investment officer at 16Rock Asset Management, emphasized that a backlog of postponed projects from the previous calendar year, particularly at year-end, is further fueling demand for issuances.

The response to decreasing market volatility has also positioned January as a favorable point for issuers to access the capital they require. There is a palpable sense of pent-up demand that was previously constrained, indicative of a landscape where missed opportunities from 2024, stemming from a tumultuous economic climate, are now being rapidly addressed. Issuers are evidently eager to navigate out of the constraints of the previous year and initiate critical infrastructure projects.

Dissecting the particulars of the January issuance offers enlightening insights into market behavior. Tax-exempt issuance accounted for $31.45 billion, a modest increase of 3.3% from the previous year, while taxable issuance surged by an impressive 36.7% to $1.849 billion. New-money issuance, critical for launching fresh projects, experienced a staggering 51.4% increase, reflecting a strong commitment among issuers to advance new capital initiatives. By contrast, the trend in refundings (the reissuing of bonds to take advantage of improved market conditions) demonstrated a decline of 40.4%, possibly signaling a strategic shift in priorities towards new projects over refinancing existing obligations.

Furthermore, revenue bonds, often crucial for funding specific projects, saw a 14% rise, paralleling an uptick in general obligation bond sales, which rose by 4.4%. Notably, negotiated deal volume increased markedly, underscoring a trend towards more tailored bond offerings that appeal to specific investor interests.

Geographically, California emerged as the leader in issuance, accounting for a remarkable $6.371 billion, a 12.6% increase compared to the previous year. Texas and Florida closely followed, with comparable growth metrics reflecting regional resilience and financial strategy in mitigating risks. Significantly, the state of Ohio reported an astonishing increase of 3,631.4%, emphasizing the volatility and opportunities presented within specific state markets.

Forecasts for the remainder of 2025 suggest not only continuity in this upward trend of issuance but also the potential for year-on-year growth matching or exceeding the total issuance observed in 2024. Experts remain optimistic that the combination of deferred project initiation and an influx of federal infrastructure support will continue to bolster municipal bond demand.

As January’s municipal bond issuance reflects a confident and proactive market stance amid uncertainties, stakeholders are left to contemplate the balance of opportunity and risk inherent in the current landscape. With dynamics shifting and mixed local fund inflows tempered by rising rates, the municipal bond market promises to be an essential focal point for both issuers and investors through 2025. By actively navigating the challenges posed by economic and policy shifts, issuers will likely capitalize on this momentum to drive essential projects necessary for community advancement and growth.