The landscape of municipal finance is currently undergoing a pronounced transformation, particularly in the realm of Build America Bonds (BABs). Amid swirling market conditions, escalating interest rates, and shifting economic motivations, the activity surrounding BAB redemptions has experienced a marked slowdown. Despite these challenges, a number of issuers are indicating their intent to call back their BABs before the year’s conclusion, suggesting that insights into issuer behavior are crucial for understanding the broader market implications.

As we entered 2024, approximately $14.9 billion of BABs had been called, with expectations set for an additional $938.3 million to be redeemed, according to J.P. Morgan. Notably, 39 issuers have executed transactions aimed at refunding their outstanding BABs this year. This activity contrasts with early predictions that suggested up to $30 billion in BABs could be eligible for early redemption following a favorable court ruling granting issuers access to extraordinary redemption provisions (ERPs).

The decision to refund outstanding BABs is heavily contingent on economic rationality. According to Nick Venditti, the head of Municipal Fixed Income at Allspring, issuers are likely to only pursue refunds when it is financially advantageous, particularly when interest rates significantly undercut the existing rates of the bonds. The current economic environment, characterized by a 10-year U.S. Treasury yield at 4.27%, illustrates the complexity that issuers face in finding viable savings opportunities compared to earlier fiscal conditions.

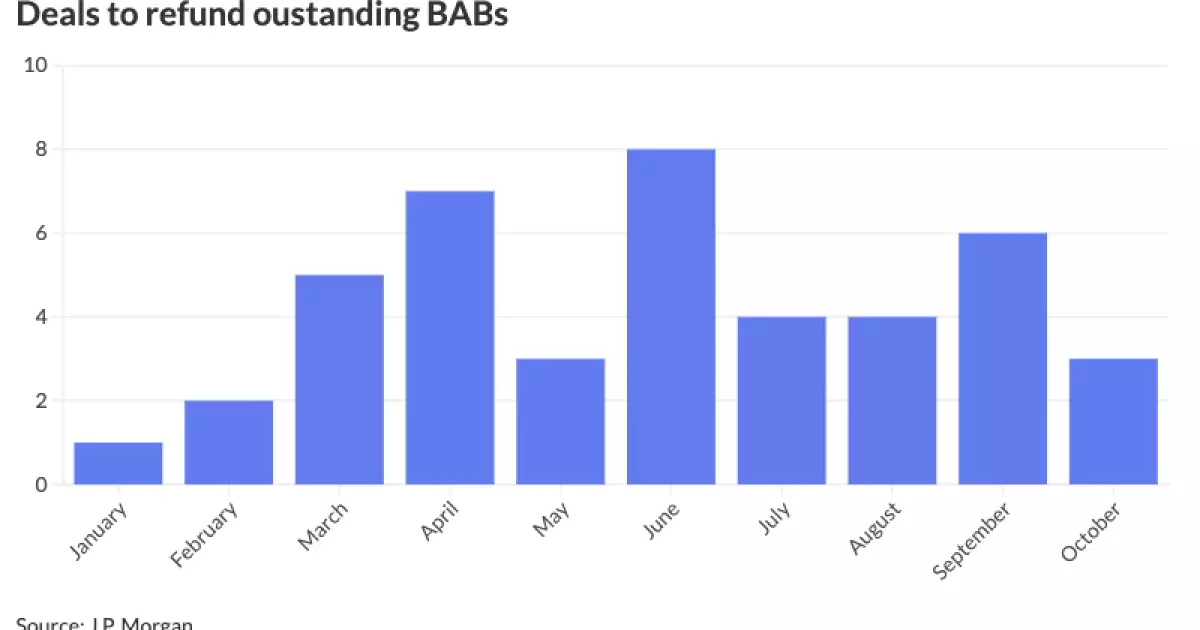

Data reveals fluctuations in the volume of BAB refundings throughout the year. The first quarter of 2024 saw a lackluster start, but there was a notable surge in the second quarter with eight deals recorded in June alone. This momentum has since tapered off, with a dip in the third quarter. Notably, the Los Angeles Unified School District initiated the most substantial single refunding transaction of nearly $2.9 billion in late April. This trend underscores the dependence of BAB refunding activities on broader economic health and market sentiment.

Market perceptions are intrinsically linked to refunding behavior. James Pruskowski, chief investment officer at 16Rock Asset Management, emphasized the impact of rising interest rates on the urgency for bond refundings. He further pointed out that the initial concerns over ERP language in bond indentures have lessened, allowing issuers to recognize that market difficulties could present opportunities in other areas.

Broader volatility within the market has resulted in strategic shifts from issuers. A illustrative case is the Ohio Water Development Authority, which opted to withdraw a $102.02 million refunding deal due to concerns over minimal projected net present value savings amidst tumultuous market conditions. Mike Fraizer, the authority’s executive director, indicated that the decision to withdraw was made to optimize future savings. This decision reflects a broader hesitation among issuers to commit to BAB refunds without confidence in market stabilization.

It is also noteworthy that even amid market uncertainties, several issuers have remained resolute in their plans to refund outstanding BABs. For instance, the Regents of the University of California moved forward with its call of outstanding BABs despite potential legal ramifications—a decision affirming the contention that many entities see value in pushing ahead with these transactions.

Current investor sentiment towards BABs is precarious. According to Venditti, outstanding BABs are trading at suppressed values as many investors are deterred by the inherent call risks associated with these bonds. Institutional investors, particularly insurance companies, are gravitating towards taxable munis that better match their portfolio objectives. The landscape of BABs has shifted dramatically, leading Venditti to describe them as “almost uninvestable” due to newly established market dynamics.

Conclusion: As the trajectory of Build America Bonds continues to unfold, the interplay between interest rates, economic conditions, and issuer decision-making will remain critical in shaping the future of municipal financing. Investors and issuers alike must navigate these complexities to find sustainable paths forward. The adjustments seen in the BAB market are indicative of a broader trend where financial decisions are increasingly being dictated by external economic pressures, raising important considerations for all stakeholders involved in the municipal bond ecosystem.