The municipal bonds market is currently experiencing a firmer stance as traders prepare for a smaller new-issue calendar following recent fluctuations in U.S. Treasury yields. With equities showing a mixed performance, market participants find themselves grappling with the implications of macroeconomic reports, which have introduced additional complexities into bond trading strategies. A recent employment report and the highly anticipated consumer price index (CPI) have notably influenced the dynamics of the Treasury market, leading to a phenomenon known as “bear steepening” in the yield curve. Analysts at Bank of America (BofA) have indicated that volatility in rates largely overshadowed recent tariff announcements, hinting at a shift in market focus towards inflationary pressures.

The aforementioned CPI report has ignited market reactions, compelling investors to adjust their positionings as volatility alters expected yield trajectories. Barclays strategist Mikhail Foux emphasized the challenges posed by abrupt movements in Treasury rates tied to inflation issues and tariff developments. As investors brace for continued fluctuations, BofA analysts advocate preparing for a trading environment characterized by range-bound Treasury yields until definitive trends in inflation emerge.

Looking ahead, the issuance calendar for municipal bonds appears subdued, projected at approximately $5.5 billion for the upcoming week, due to ongoing holiday-related reductions in activity. Despite this temporary dip, analysts remain optimistic about the overall supply dynamics for February, with a current visible supply level of around $10.42 billion, indicative of healthy market conditions. The balance of supply and demand continues to show robust strength, driven by large redemption volumes and consistent mutual fund inflows.

BofA’s strategists highlighted that strong demand remains a crucial factor in the municipal market, as the influx of investor capital regularly overwhelms the current levels of issuance. They noted a recent revival in refunding volumes, supported by the favorable market rally executed before the CPI report, showcasing robust investor interest. This increase helped yield a commendable $4.2 billion in refunding month-to-date alone, a significant bounce-back from previous issuance levels.

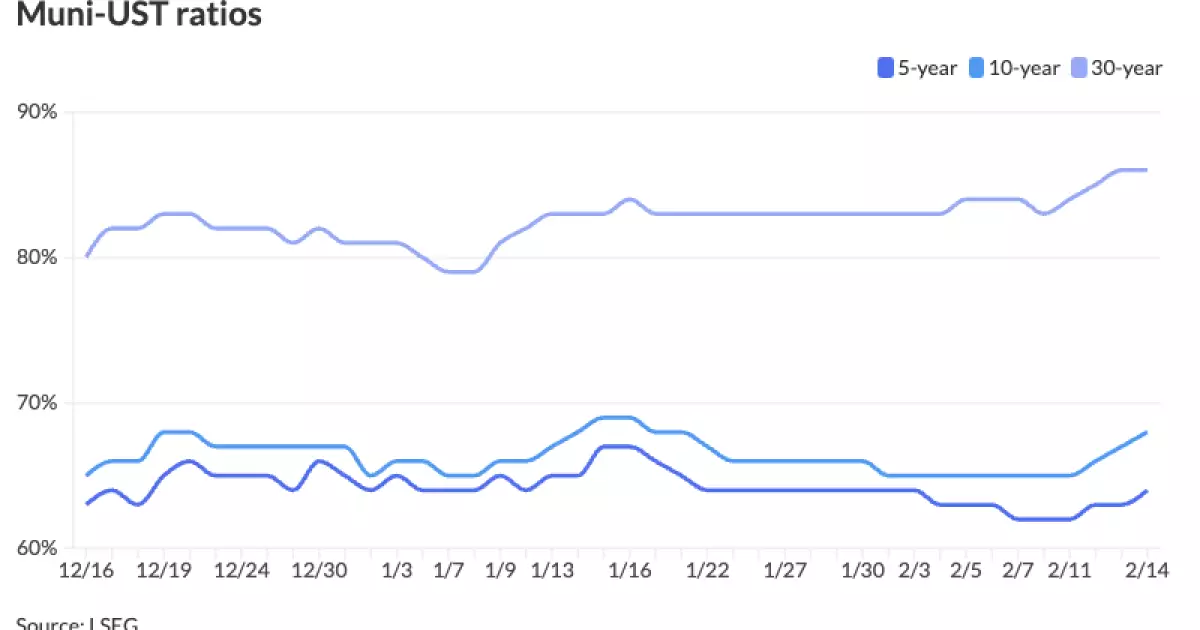

Recent data underscores an evident decline in municipal (muni) yields, with the 10-year muni yield decreasing by approximately 35 basis points during a span from mid-January to early February. However, trends may indicate a slight softening in muni-to-U.S. Treasury (UST) ratios, as observed in comparative analysis data. Speculations suggest that the two-year ratio stands at around 63%, while the 10-year ratio hovers around 68%. Such movements imply shifting investor sentiment and aversion towards prolonged duration risks, as evidenced by the steepening of the AAA yield curve.

Investor caution is further reflected in the flattening ratios across various terms, with the risk appetite appearing tempered due to overall market uncertainties. For example, the 1s10s AAA slope exhibited a significant change, moving from a deeply inverted state of -70 basis points last year to a steeper slope of 37 basis points currently. Such developments underscore an essential recalibration in investor expectations and highlight an ongoing search for yield in a fluctuating interest rate milieu.

The new issuance landscape is set to gain momentum with expectations of approximately $5.535 billion, featuring a diverse range of negotiated and competitive deals. Noteworthy among these is a substantial $526 million offering from Miami-Dade County for airport revenue bonds, which signals substantial interest in infrastructure development, especially in the economic recovery context post-pandemic. This prioritization reflects a broader trend of municipalities seeking to capitalize on financing opportunities that underscore growth and revitalization.

Additionally, several other notable issuances include $500 million of taxable Economic Development and Infrastructure programs revenue bonds from the Pennsylvania Economic Development Financing Authority. Crucially, the competitive calendar also adds depth, with Guilford County leading with $570 million in general obligation (GO) school bonds. Such a variety illustrates the continued vitality of the municipal bond market as a funding mechanism for essential public projects, which is crucial for maintaining the fabric of community development.

In closing, the municipal bond market presents a complex yet invigorating picture, marked by both opportunities and challenges amid rate volatility. The need for investors to adopt adaptive strategies in the face of unpredictable yield movements cannot be overstated. As the end of February approaches, market participants are urged to remain vigilant, keeping an eye on key economic indicators while positioning themselves to capitalize on projected changes. Only with a thoughtful approach can they navigate the intricacies of the municipal bond landscape to capture potential value and manage risks effectively in the months ahead.