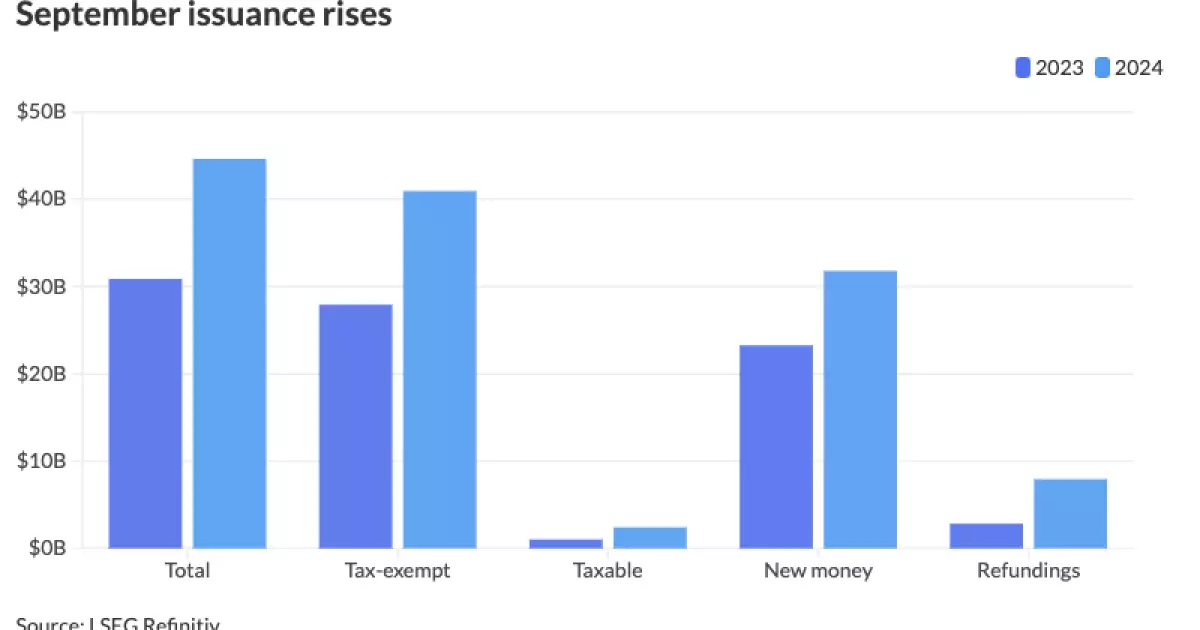

As we navigate through 2024, the bond issuance market is experiencing a remarkable surge that positions it to potentially set new historical records. Data from LSEG reveals that September marked yet another impressive month in the market, highlighted by a 44.5% increase in issuance compared to the previous year. This growth can largely be attributed to state and local governments organizing larger deals, primarily fueled by new-money requirements. Year-to-date figures show a total issuance of approximately $380.423 billion, only slightly below the complete total for 2023 of $384.715 billion. With only three months left in the year, a significant spike—over $104 billion—would be required to surpass the 2020 record of $484.601 billion, presenting both challenges and opportunities for issuers.

The issuance for September itself reached an impressive $44.628 billion across 752 deals, thereby surpassing the 10-year average of $35.679 billion in the process. This remarkable activity in the bond market signals a renewed confidence among issuers, particularly as many continue to navigate the uncertainties brought by dwindling pandemic aid and the upcoming elections.

Further examination reveals that the ongoing high volume can be traced to two critical elements: the conclusion of COVID-related financial assistance and a proactive stance by issuers aimed at preempting election cycle uncertainties. The expiration of pandemic funding demands an urgent return to the municipal market by issuers who need to address their new-money needs, as delineated by Drew Gurley of Siebert Williams Shank. This urgent need is tempered by the reminder of the volatile market reactions observed during previous election years.

Kim Olsan, a senior fixed income portfolio manager at NewSquare Capital, asserts that the current landscape is markedly more favorable compared to 2023, where issuance levels frequently dipped. The commitment from investors and reasonable financing rates have spurred an uptick in considerable deals. In September alone, tax-exempt issuance saw a 46.6% year-on-year rise, reaching $40.944 billion. In parallel, taxable issuance witnessed an even more astonishing increase of 135.6%, demonstrating a robust appetite for different types of bonds in the market.

One of the most notable trends in the current issuance cycle is the uptick in mega deals, with issuers now regularly bringing forth billion-dollar bonds. Historically, such instances were sporadic, but today brings a new norm where multiple billion-dollar offerings can appear within the same week. Highlights from recent mega deals illuminate this trend, including substantial offerings like $1.6 billion from Washington, D.C., and similarly sized offers from Texas and New York City authorities.

The acceptance and demand for these significant offerings underline a growing sophistication and confidence among both issuers and investors, as Gurley points out. The relative success of these large transactions alludes to liquidity in the market, given that capital appears ample and issuers are not hesitant about venturing into sizable offerings.

Navigating Election Cycles and Future Projections

The confluence of financial imperatives and electoral considerations has stimulated a flurry of activity among bond issuers. Historically, election cycles have placed considerable pressure on the bond market, resulting in volatility that prompts many to preemptively enter the market to mitigate risks. Notably, previous election years like 2016 and 2020 yielded sizable issuances in the last quarter, reinforcing an established pattern.

As we look forward, a slight decrease in issuance is anticipated leading up to the election date in November. However, there appears to be a willingness among issuers to capitalize on post-election opportunities, aligning with historical precedents. The initial weeks of December could yield notable activity, easing into the year’s end as pressing borrowing needs persist.

Examining the regional breakdown of bond issuance, Texas retained its position as the top state by a considerable margin, accounting for $56.138 billion year-to-date, followed closely by California and New York. The notable increases across states underscore a broader trend where municipal issuances are ramping up at a pace that contrasts sharply with previous years.

Ultimately, the current trajectory of the bond market reveals a landscape undergoing profound transformation, driven by the interplay of renewed issuer activity and a supportive investor environment. The coming months will be pivotal in determining whether 2024 can indeed deliver on the promise of record-setting totals or if external factors will once again alter the course of this dynamic market. As the data unfolds, it becomes clear that the narrative is not just about statistics; it reflects a broader economic context rich with implications for municipalities, investors, and the market at large.