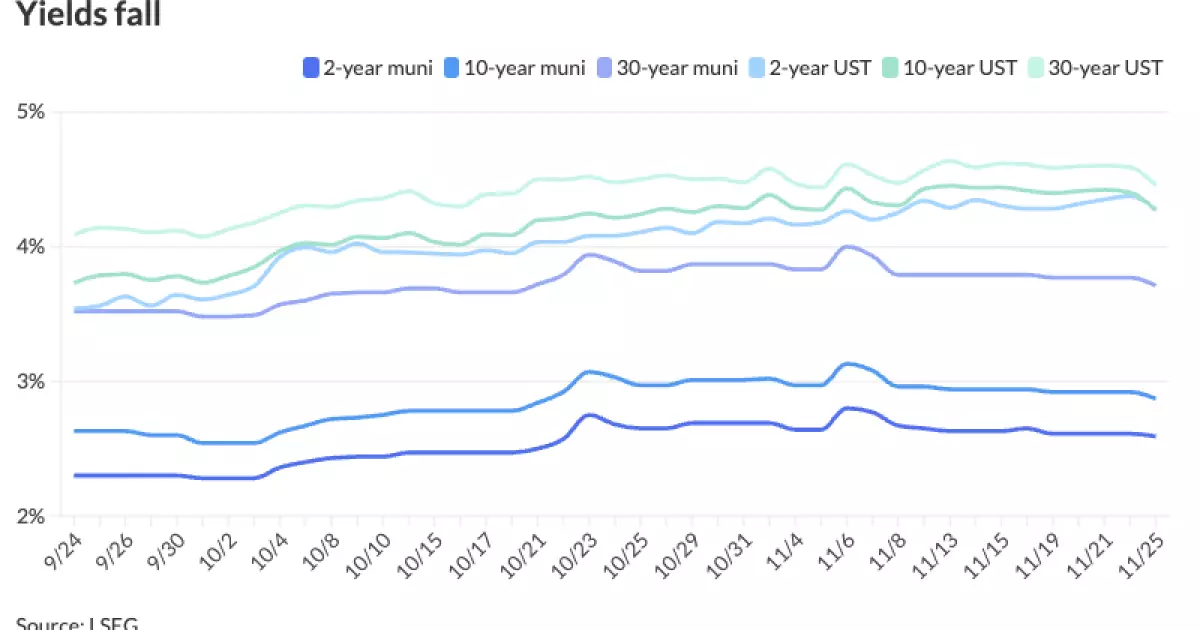

As the financial landscape shifts in response to various economic factors, the municipal bond market is also adapting in significant ways. Recent developments indicate a noteworthy decline in municipal bond yields alongside a rally in U.S. Treasury yields. This dynamic has profound implications for investors, policymakers, and the broader economic environment.

The announcement of Donald Trump’s Treasury Secretary pick has spurred mixed reactions in the financial markets. Scott Bessent, a prominent hedge fund manager, has been nominated for the role, which some analysts view as a stabilizing force in the Trump cabinet. According to a UBS report, market responses suggest that Bessent’s choice is perceived as a commitment to responsible fiscal governance. The underlying concern, however, lies in the potential inflationary risks tied to Trump’s economic policies. Analysts from UBS predict that the anticipated policy outcomes may not be as inflationary as initially feared, which could stabilize the U.S. Treasury yields over the coming years, despite recent volatility in financial markets.

In contrast to October’s downturn, where municipal bonds lost 1.46%, November has brought a revitalization of performance. Year-to-date returns are rebounding, with yields climbing up to 0.88% for municipals, thus pushing cumulative returns to 1.69%. This improvement can be attributed to robust demand for tax-exempt income, which has emerged as a key driver for the municipal market’s relative outperformance. Daryl Clements, a Portfolio Manager at AllianceBernstein, notes that tighter after-tax spreads contribute to this positive trajectory.

Despite a backdrop of rising municipal yields—sometimes reaching seven basis points—investor interest remains strong. Interestingly, while high-yield munis are proving lucrative this month, taxables lag slightly behind. These shifts reflect broader trends and investor sentiment tied to tax policy changes and perceived market risks.

A critical consideration is how municipal bonds are currently priced relative to U.S. Treasuries. As of the latest data, the ratios between municipal bond yields and UST yields have hit significant benchmarks, with the 30-year ratio peaking at 83%. This trend implies that municipal bonds are becoming relatively more expensive compared to their Treasury counterparts, particularly in longer durations. Some experts are cautioning that, even as munis continue to outperform, the price differential may present challenges for municipalities when issuing new debt, especially in longer-term bonds.

Looking ahead in the municipal market, supply is projected to dip as year-end approaches. This reflects a typical seasonal pattern of reduced issuance, but there have been hints of a rebound in the initial weeks of December, with larger deals already on the horizon. The Greater Orlando Aviation Authority, for example, is expected to price $843 million in airport facility revenue bonds, while the State of Hawaii is preparing to issue $750 million in taxable general obligations.

Notably, recent upgrades among municipal issuers are setting the stage for a healthier loan environment. The market has shown a remarkable capacity for absorbing supply, with substantial inflows—$1.288 billion in the latest week alone—indicating strong demand from investors, especially those focused on longer-dated bonds.

The trade activity over the recent weeks suggests a pivot in investor preferences. A surge in customer bids for maturities of ten years and shorter highlights shifting focus, with increased purchases in the 10- to 20-year range. This indicates a cautious optimism among investors amid ongoing market fluctuations and economic uncertainty. Conversely, short-duration funds are witnessing outflows, hinting at a segmented market where risk appetite diverges based on factors like duration and yield perspectives.

Overall, the municipal bond market reflects an evolving landscape characterized by complex interactions between political developments, fiscal policies, and economic indicators. As we approach the end of the year, investors will be watching closely for any signs of further market evolution, particularly amid discussions surrounding interest rates and inflation. The ongoing performance of municipal bonds suggests that, while some caution remains warranted, there are also unique opportunities for growth and yield enhancement within this segment of the market.